Did you know that over 60% of businesses struggle with cash flow issues directly linked to poorly optimized payment processing setups? What seems like a minor inefficiency can actually snowball, causing cascading disruption in your business’s financial stability, limiting growth, and trapping working capital

A Startling Look at Payment Processing Cash Flow Disruption

"Recent studies show that over 60% of businesses face cash flow issues due to inefficient payment processing setups."

Payment processing cash flow is more than just moving money from a sale through your accounts—it's the lifeblood that keeps your business operational and enables growth. When the payment process is slow, opaque, or riddled with errors, your working capital suffers. These disruptions increase the risk of missed opportunities and late fees and, in severe cases, can threaten the very existence of your company. Whether you're accepting credit card payments in-store, handling virtual card payouts online, or processing bank transfers, a poorly designed payment system or outmoded payment processing system leads to expensive bottlenecks.

Imagine delayed card payment settlements resulting in unpaid invoices, or outdated payment methods causing customers to abandon transactions. Each hiccup in the payment workflow expands into wider cash flow gaps and compounding losses in both revenue and customer satisfaction. By solving these issues proactively, businesses can ensure their working capital remains healthy, paving the way for confident decision-making and seamless growth.

What You'll Learn: Key Insights About Payment Processing Cash Flow

Understand how payment process inefficiencies stunt working capital and cash flow.

Recognize the warning signs of poor payment processing systems and solutions.

Identify actionable steps to optimize payment solutions and methods.

Understanding Payment Processing Cash Flow: Fundamentals Every Business Needs

Defining Payment Processing and Its Link to Cash Flow

At its core, payment processing is the series of steps a business takes to accept, verify, and transfer funds from a customer's payment to the company’s bank account. Every payment method—from card payments to digital wallets—relies on a secure, streamlined set of steps for the transaction to occur. Yet, if any part of this payment process is inefficient or outdated, it slows access to vital funds, impeding cash flow and reducing available working capital. In today's fast-paced environment, customers expect instant gratification, and any delay in resolving payment system issues can seriously damage not only the company's liquidity but its reputation as well.

For most businesses, payment processing cash flow involves managing multiple moving parts: customer purchase, authorization, transfer, and finally, settlement into company accounts. A friction-filled or error-prone payment processing system disrupts this journey, increasing processing costs and decreasing customer satisfaction. As a result, companies that don’t review and optimize their payment solutions risk falling behind—both financially and competitively.

Addressing these challenges often starts with a thorough review of your current payment workflows and identifying where inefficiencies are costing you most. For a step-by-step approach to evaluating and upgrading your payment systems, explore our guidance for building a strong small business, which covers practical strategies for strengthening your financial foundation.

How the Payment Process Directly Impacts Cash Flow

The payment process directly affects when—and how much—money your business can actually use. Delays in authorization, settlement, or even reconciliation within your accounting software create gaps in available working capital. These delays often stem from disjointed payment systems, outdated technology, or inefficient approval flows. Each hour or day lost in processing time means capital is inaccessible for payroll, new inventory, or unforeseen expenses.

Furthermore, processing solutions that lack real-time updates can mislead business owners into believing they have more liquidity than they truly do. Inaccurate cash flow forecasting leads to overcommitment and exposes businesses to the risk of bounced checks, missed payments, or rushed borrowing under unfavorable payment terms. The only way to mitigate this is by implementing modern and connected payment processing solutions that provide end-to-end visibility and speed.

Working Capital, Payment Systems, and Payment Processing Cash Flow

Working capital is the difference between a company’s current assets and current liabilities. For businesses of all sizes, the fluidity of moving funds—from payment initiation all the way to bank settlement—determines how agile that company can be in seizing new opportunities. Inefficient payment processing systems act like a bottleneck, holding onto funds that could be put to productive use.

By improving the payment system workflow, organizations see shorter cycles for card payment settlements and better forecasting accuracy. This leads to optimized staffing, timely vendor payments, and more strategic growth decisions. Conversely, fragmented or manual processing systems steadily eat away at the resources needed to sustain a healthy cash flow and resilient working capital management.

The Role of Card Payment and Payment Methods in Payment Processing Cash Flow

The choice of payment methods has a significant impact on payment processing cash flow. Card payments—whether credit card, debit, or virtual card—often settle faster than checks or traditional invoices. However, they may come with higher processing costs. Meanwhile, instant mobile payment options and digital wallets can provide both speed and convenience but must be integrated securely in your payment system.

Businesses that fail to offer a variety of payment options limit how quickly they can receive funds. On the other hand, adopting too many disconnected payment methods creates reconciliation headaches, bloating administrative time and creating opportunities for costly errors. The optimal solution is a well-integrated, modern payment processing solution that matches your customer expectations while ensuring efficient cash flow.

Common Payment Processing System Pitfalls That Hurt Cash Flow

Inefficient Payment Solutions: Delays, Errors, and Hidden Costs

Outdated payment system limitations

Lack of digital payment methods

Disconnected accounting software

Poor customer experience during payments

Many businesses are stuck with outdated payment systems that simply can't keep up with modern commerce. These systems introduce avoidable delays, frequent processing errors, and sometimes, hidden fees that drain profit margins. Relying on old terminals or manual invoice processes means customers might encounter friction when they try to make payments. Each failed or delayed transaction not only results in lost sales but also creates an administrative burden, as staff scramble to fix errors and re-enter payment information into siloed databases.

The absence of digital or mobile payment methods makes the experience worse for both customers and team members, stalling settlements and stretching out the cash flow timeline. Without automation through accounting software or integration between different processing systems, reconciliation becomes a manual, error-prone task that further exposes the business to missed or duplicate payments and compliance risks.

Processing System Issues: The Ripple Effect on Cash Flow

A poorly configured payment processing system doesn't just delay receipts—it can send shockwaves through your organization. When processing system dashboards are overly complex or lack real-time clarity, confusion grows among both staff and management. Decisions are then based on inaccurate assessments of working capital and liquidity, risking overextension or unexpected shortfalls. Each processing solution that fails to communicate seamlessly with accounting or inventory modules causes costly ripple effects.

These issues aren’t isolated to accounting—they impact every department, from sales to procurement. A locked or delayed payment process can create cash flow gaps, stall critical projects, or lead to missed discounts due to late vendor payments. Forward-thinking businesses understand that stable working capital depends on eliminating these ripple effects by investing in intuitive, modern payment processing solutions that grow with them.

Slow Payment Terms and How They Drain Working Capital

Payment terms define how long after a sale a business receives its money. Operating on extended payment terms or with clients who repeatedly delay can strangle cash flow, especially if those funds are crucial for covering operating expenses. This often occurs for service-based businesses or B2B companies with recurring invoices, where slow settlements directly restrict available working capital.

If your processing system cannot support flexible payment options like immediate ACH transfers or digital wallet settlements, you’re locking your cash behind walls. Automation and frequent reminders can help speed up payments, while offering incentives for quick card payment or mobile transfers fosters a cycle of healthy liquidity.

Fragmented Payment Methods and Clunky Systems

Fragmentation happens when a business uses many different payment methods or disconnected platforms, making reconciliation and cash flow forecasting nearly impossible. This leads to duplicated data entry, missing payments, or even fraud exposure. Clunky payment processing systems only complicate matters: for each unique channel—be it in-store, mobile, or online—you may be managing a separate portal or workflow.

Effectively, instead of streamlining the payment process, these systems create more work, slow down collections, and create new, costly bottlenecks. The solution lies in consolidation: integrating your payment solutions to gain a holistic view of incoming and outgoing funds, streamline operations, and maximize your operational cash flow.

The Workflow of Payment Processing and Its Effect on Payment Processing Cash Flow

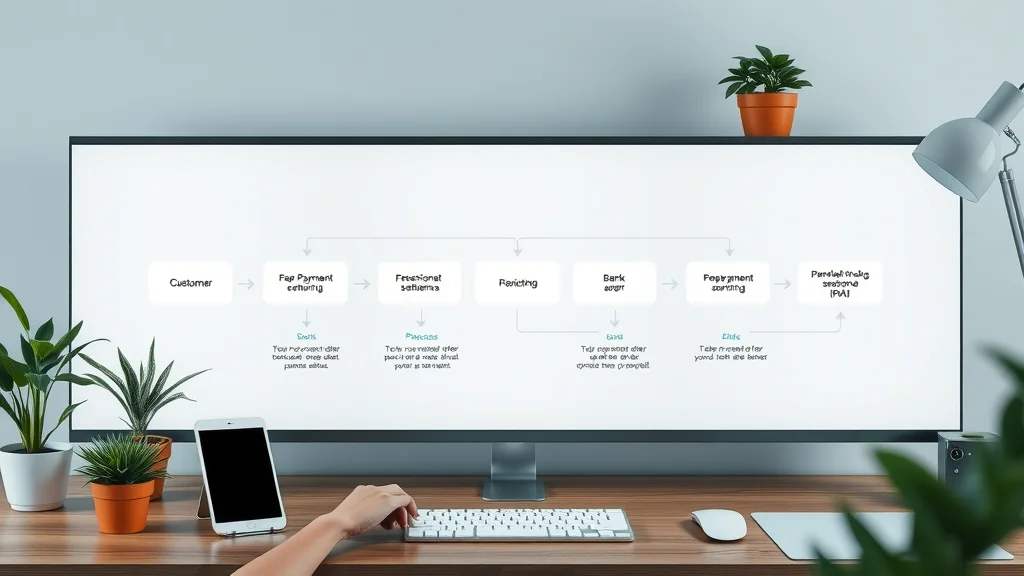

What is the Workflow of Payment Processing?

Step-by-step journey: from payment initiation to settlement

Key players in the payment processing system

The typical payment processing workflow starts with payment initiation (when a customer provides payment details), followed by authorization (approval by banks or card networks), clearing and settlement (moving funds between accounts), and ends with reconciliation in your accounting software. Key participants include the customer, merchant, payment gateway, merchant bank, acquiring bank, and card networks. Any inefficiency—be it a slow internet connection, data entry error, or bank hold—can extend this timeline and hurt cash flow.

Companies with automated, integrated payment systems make this journey seamless, meaning money is accessible almost instantly and records are automatically updated. Those with fragmented processing systems or lots of manual intervention, however, deal with missing funds, data discrepancies, and a prolonged wait for necessary capital.

How Workflow Inefficiencies Lead to Cash Flow Gaps

When the payment workflow is inefficient, each stage—from authorization to reconciliation—has the potential to stall, creating cash flow gaps. Manual steps increase errors and time delays, leading to missed revenue and misallocated working capital. For example, delays in batched settlements could mean waiting days or even weeks to access funds, making it hard to meet payroll, restock quickly, or pay off vendors on time.

This fragmented model also decreases customer satisfaction. A confusing or sluggish payment process can prompt abandoned carts or negative feedback, further tightening your revenue and cash flow. Businesses must re-engineer their process with automation, real-time monitoring, and seamless integration to close these gaps and drive maximum liquidity.

Comparison of Efficient vs. Inefficient Payment Processing Workflows |

||

Efficient Workflow |

Inefficient Workflow |

|

|---|---|---|

Cash Flow Impact |

Funds accessible within hours or next business day, faster reinvestment, fewer shortfalls |

Funds delayed for several days/weeks, bottlenecks, higher risk of negative balances |

Working Capital |

Optimized, predictable, supports business growth and agility |

Constrained, unpredictable, increases need for emergency borrowing |

Customer Experience |

Frictionless, boosts loyalty, encourages repeat sales |

Frustrating, causes cart abandonment, damages reputation |

Analyzing the Five Steps of Transaction Processing in Payment Processing Cash Flow

What are the 5 Steps of Transaction Processing?

Authorization

Batched Settlement

Clearing

Funding

Reconciliation (within accounting software)

The five key steps in the payment process underpin every successful transaction and healthy cash flow:

Authorization: Approval from issuing bank or service, confirming available funds and legitimacy.

Batched Settlement: Grouping transactions for processing, impacting when money moves.

Clearing: Financial institutions verify and transmit payment data for both sides.

Funding: Funds actually move into the merchant’s bank account.

Reconciliation: Transactions are matched in accounting software, closing potential gaps and ensuring accuracy.

A break or delay at any step expands the time it takes to clear card payments and receive funds, multiplying the risks of errors and shortfalls in working capital.

How Each Step Influences Payment Processing Cash Flow and Working Capital

Each stage plays a fundamental part in controlling your payment processing cash flow. Issues during authorization can result in declined payments and lost sales opportunities. Slow or inefficient batched settlements can trap much-needed revenue, with delayed clearing and funding translating into real cash shortages. Finally, insufficient reconciliation processes—especially those not connected with digital accounting software—mean discrepancies may go unnoticed until it’s too late.

The takeaway: Businesses should review each of these steps, automate where possible, and ensure each processing solution is tightly integrated. This safeguards the accuracy and timeliness of available working capital for payroll, inventory, and growth.

The Relationship Between Payment Methods and Payment Processing Cash Flow

Diverse Payment Options: Pros and Cons for Your Cash Flow

Credit card payments

Bank transfers

Digital wallets

Instant payments

Offering a range of payment options enhances customer satisfaction and can improve cash flow by shortening settlement times. For example, credit card and instant payment methods (like Zelle or Venmo) generally provide quicker access to funds compared to checks or wire transfers. Digital wallets satisfy tech-savvy customers and may reduce fraud, but require up-to-date terminals and tighter security.

Each payment method comes with trade-offs. Card payments, while fast, incur higher processing costs than bank transfers. Meanwhile, fragmented solutions can increase administrative complexity if not managed effectively. The best approach is to find an optimal mix that meets customer needs while minimizing settlement delays and fees, keeping your payment processing cash flow streamlined.

How to Improve Payment Processing Cash Flow With the Right Payment Solution

Improving payment processing cash flow starts with selecting modern, customer-focused payment solutions. Look for systems that seamlessly handle multiple payment methods, integrate directly with accounting software, and offer real-time reporting. Automation of reminders, instant card payment processing, and simplified reconciliation all decrease friction, speed up settlements, and maximize available working capital.

Consider investing in platforms that balance speed with security—offering both rapid settlements and robust fraud protection. Tailoring payment options to your customer base also promotes higher customer satisfaction and retention. By taking a strategic approach to payment processing solutions, you’ll ensure liquidity isn’t an afterthought but a competitive advantage.

Payment Solutions and Systems: Choosing What’s Right for Healthy Payment Processing Cash Flow

Evaluating Modern Payment Processing Systems for Better Cash Flow

Start by looking at speed: do funds settle in hours or days? Then assess flexibility—can your customers use preferred payment methods like credit card, digital wallets, and mobile pay? It’s also crucial to consider support for recurring payments and how robust the customer experience is throughout the payment process

The most effective payment solutions offer full integration with accounting software, boosting accuracy and visibility. Evaluate whether the system can scale as you grow and if it provides actionable insights into cash flow and working capital. Avoid platforms that require manual reconciliation or lack transparency—these will only extend cash flow gaps over time.

Integrating Payment Solutions with Accounting Software for Seamless Payment Process

Simplifying reconciliation of payment transactions

Boosting overall visibility and control

Integration between payment solutions and your business’s accounting software eliminates tedious manual updates and reduces the risk of human error. By syncing real-time transaction data directly into your general ledger, you not only simplify reconciliation but also enhance your oversight into available working capital. This connection enables faster, more accurate reporting and reveals critical payment trends and potential bottlenecks before they escalate.

Fully integrated payment processing systems also trigger automatic alerts for failed or pending settlements—empowering your team to take rapid action. This level of workflow automation frees up staff, speeds the payment process, and ensures maximum liquidity with minimum effort.

Impact of Customer Experience on Payment Processing Cash Flow

"A seamless payment system not only retains customers but also accelerates your working capital cycle."

The link between customer experience and payment processing cash flow can’t be overstated. A frictionless, reliable payment method encourages timely payments and repeat purchases. In contrast, convoluted or error-prone systems drive up cart abandonment and result in lost revenue. Positive experiences mean customers return and promote your brand, accelerating sales as well as your access to funds.

Optimizing every touch point—from payment initiation to confirmation and refund processing—boosts not only cash flow but also your competitive edge in a crowded marketplace.

Case Studies: How Bad Payment Processing Setup Damaged Cash Flow

Small Business Example: Payment System Bottlenecks

Consider a local restaurant that insisted on manual POS terminals and paper receipts. During peak hours, order delays and double charges became common—leading to customer complaints and lost business. The owner soon realized cash deposits were delayed by several days as reconciliation required manual entry and verification. The result was a persistent cash flow gap that affected everything from inventory restocking to payroll accuracy. After switching to an integrated, cloud-based payment processing solution, deposits arrived next business day and working capital improved instantly.

Enterprise Example: Delayed Card Payment Settlement and Cash Flow Squeeze

A large e-commerce company used multiple, non-integrated payment processing systems for domestic and international sales. Processing times varied dramatically, especially for card payments from certain regions, leaving significant revenue in limbo for days at a time. The lack of unified reporting and real-time notifications left finance teams in the dark when reconciling accounts. Migrating to a modern, multi-currency payment processing solution shaved days off settlement times and freed up millions in working capital.

Lessons Learned: Best Practices for Payment Processing Cash Flow

The lessons from these cases are clear: outdated payment processing setups lead to unnecessary cash flow gaps. The most impactful moves include adopting unified payment systems, automating manual tasks, enabling instant and digital payment methods, and consistently reviewing and optimizing payment solutions for speed, flexibility, and security. These practices not only reduce errors and costs but also empower businesses to respond swiftly to opportunities.

Step-by-Step Guide: Optimizing Payment Processing Cash Flow for Your Business

Assess Your Current Payment Systems and Solutions

Checklist of warning signs and inefficiencies

Red flags in payment terms and payment methods

Pay special attention to payment terms—are overdue accounts frequent? Are customers abandoning carts due to lack of payment options?

Monitoring these metrics provides a baseline for targeted improvements. The goal: identify where cash gets “stuck” and where adopting new payment solutions will have the biggest impact on working capital.

Implement Strategic Payment Options for Better Cash Flow

Choosing faster payment methods

Automate payment process using accounting software

Choose payment options that guarantee fast settlement, such as instant ACH, card payment, or integrated digital wallets. Consider automating invoicing and regular payment reminders to ensure prompt payment. Where possible, link your payment system to real-time accounting software—this enhances visibility and reduces the opportunity for error or fraud.

Implementing these strategic payment solutions shouldn’t disrupt current business; instead, aim for phased rollouts and staff training to ensure a smooth transition. This approach maximizes the impact on cash flow without overwhelming your team.

Watch the animated explainer video below to see how different payment processing workflows affect real businesses. Learn about common pitfalls and practical solutions for supercharging your cash flow.

People Also Ask: Answering Top Payment Processing Cash Flow Questions

What is the workflow of payment processing?

The workflow includes payment initiation, authorization, settlement, reconciliation, and reporting, each affecting speed and accuracy of cash inflow to your business.

What are the 5 steps of transaction processing?

The five steps are authorization, batching, clearing, funding, and reconciliation. Each plays a vital role in maintaining steady payment processing cash flow.

What is cash flow payment?

Cash flow payment refers to incoming and outgoing money directly linked to payments processed, determining liquidity and operational health.

What are the four types of cash flows?

Operating, investing, financing, and free cash flow are four main types, each influenced by payment processing system efficiency.

FAQs: Payment Processing Cash Flow Optimization

How can businesses quickly identify payment processing cash flow issues?

Watch for frequent reconciliation mismatches, delays between payment collection and funds availability, and high rates of abandoned transactions or rejected payments. These are classic signs your payment processing cash flow is suffering.Which payment solutions offer the fastest impact on working capital?

Integrated systems supporting instant ACH, digital wallets, and credit card payments typically provide the fastest boost in cash flow and working capital by shortening settlement times.Are integrated payment systems worth the investment for small businesses?

Absolutely. Integrated solutions improve accuracy, speed up collections, reduce errors, and provide better insights for decision-making, expanding working capital and supporting growth.How does customer experience factor into payment processing cash flow improvement?

A seamless, easy-to-use payment process increases customer satisfaction, shortens payment cycles, and reduces abandoned purchases—all of which accelerate cash flow into your business.

Key Takeaways for Improving Payment Processing Cash Flow

Bad payment processing setups create cash flow gaps and stall working capital.

Optimize payment solutions, payment methods, and use modern accounting software.

Monitor processing system workflows to ensure maximum liquidity.

Prioritize customer experience with streamlined payment solutions.

Hear from payment industry leaders and CFOs about transforming cash flow with next-gen payment systems in this in-depth interview.

Conclusion: Take Charge of Your Payment Processing Cash Flow

"Streamlining your payment process is more than an operational upgrade—it's a growth lever for your business."

Act now to modernize your payment systems and secure your company’s financial future.

If you’re ready to take your business’s financial health to the next level, don’t stop at optimizing payment processing alone. Building a resilient company means understanding the broader legal and operational strategies that support sustainable growth. Discover actionable advice and foundational steps for long-term success in our comprehensive resource on building a strong small business. By combining robust payment systems with sound business practices, you’ll be well-positioned to navigate challenges and seize new opportunities with confidence.

Write A Comment